Posted by Marc Rowson, senior vice-president at Legal Futures Associate Lockton Companies LLP [1]

Rowson: Insurers want firms to take out separate cyber insurance

Since abolition of the common renewal date, practices have been free to choose when to renew their professional indemnity insurance (PII). We estimate that around 30-40% of the profession now renews between March and April.

As a result, it has paved the way for a ‘secondary’ renewal season, with insurers and brokers alike preparing for a busy six weeks.

For those renewing annually, this period serves as a painful reminder. It was towards the end of this secondary peak period last year that lockdown measures across the country were first introduced, and insurers and practices alike were having to deal with the challenges presented by a lockdown, along with finalising PII renewal arrangements.

The traditional PII market for solicitors falls in October, and the conditions experienced in 2020 were tough. As we approach the spring of 2021, circumstances are unfortunately unlikely to improve, with all leading insurers looking to push further rate increases across their portfolios.

Primarily, these increases come as a result of a sustained period of softer market conditions in the years prior that resulted in insurers failing to build up sufficient reserves to accommodate the increasingly severe claims they are now seeing.

As such, numerous notable losses are now serving as a catalyst for premiums increasing.

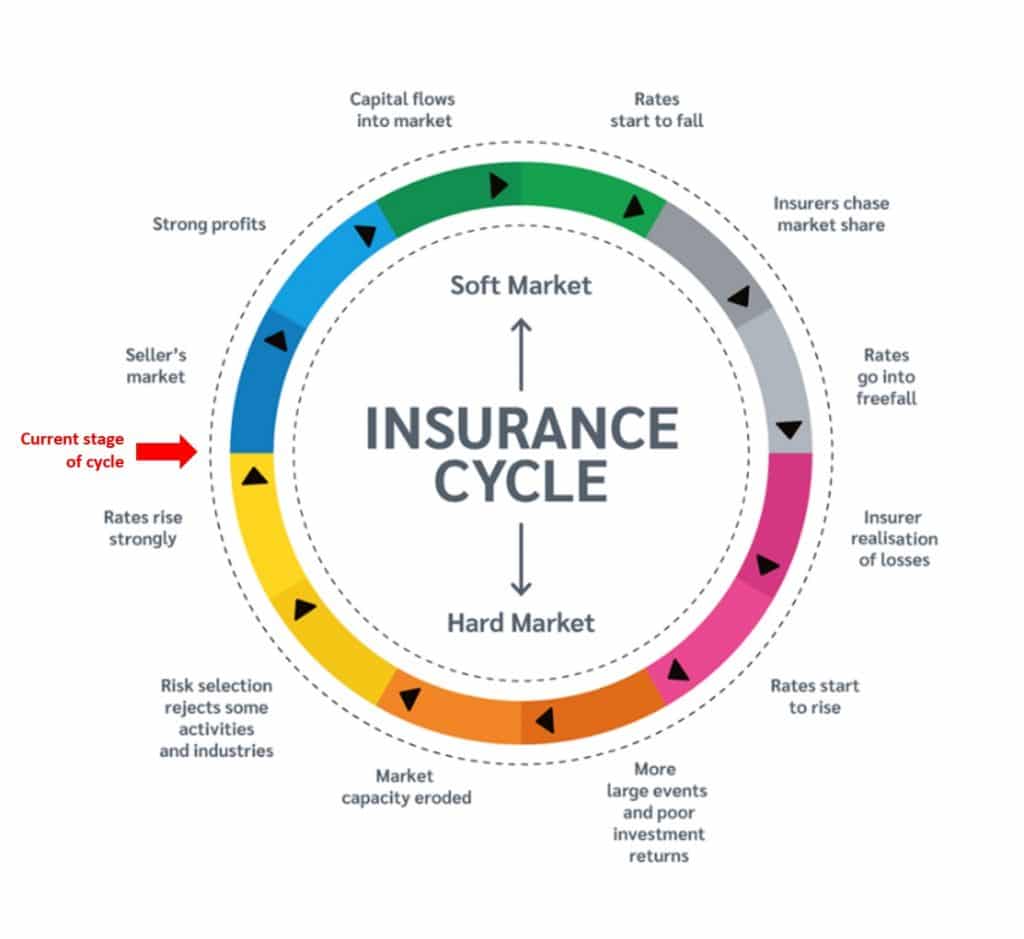

The diagram below articulates the varying stages of the insurance cycle, with the red arrow indicating our current position.

Right now, we’re experiencing what is very much an insurer’s market, with sharply rising rates. History dictates to us that periods of harder market conditions are usually much shorter than that of softer conditions, demonstrated on the right of the diagram. We can therefore be hopeful that these difficult circumstances won’t last too long.

While there are already signs of new capital entering the wider Insurance market, this has yet to be encountered in the solicitors’ PII space. Therefore, for the purpose of forthcoming renewals, it is important for practices to be aware of what to expect and how to best prepare.

Premiums are not the only aspect of the upcoming renewals to be impacted. For practices that buy above the compulsory limit of indemnity, greater clarity of coverage is expected, with insurers excluding first-party losses suffered by the insured as a result of cyber incidents from excess layer policies, and introducing affirmative language to this effect.

Insurers’ rationale is that this cover should be protected by a cyber-insurance policy, not a professional indemnity policy.

The primary layer remains unaffected currently, albeit insurers are lobbying the Solicitors Regulation Authority (SRA) for changes in the minimum terms and conditions (MTC) in order to accommodate such changes. The SRA’s current position is that it is consulting on proposed changes to the MTC, with a decision to follow in the coming months.

In addition to the introduction of affirmative language, the past year has also seen a trend whereby certain primary layer insurers request that their insured practices purchase a cyber-policy in addition to their PII, so that the former will be the first policy to ‘trigger’ in the event of a cyber-incident and loss.

We anticipate more insurers will be introducing such measures if there is no forthcoming change in the MTC.

The fact the MTC will not change before April means some insurers will continue to require personal guarantees for LLPs or incorporated practices, providing a commitment that any unpaid excess or run-off premiums will be met by the directors, even in the event of a firm ceasing to trade.

Insurers that have implemented such policies remain concerned about the uncertain economic environment, as well as the issue of unpaid debts experienced in recent years where firms have unfortunately failed.

I must stress that, despite the challenging conditions, there is still an active commercial market, albeit the conditions are somewhat tougher and more challenging, including the working environment, with the vast majority of Insurers continuing to work remotely.

While it’s possible that there will be some return to normal life in the coming weeks, the insurance industry is likely to continue working remotely throughout this forthcoming renewal period. Ten and a half months of experience tells us that this working environment will slow down the underwriting process considerably, so obtaining terms from insurers could take longer.

If you haven’t started the process, we’d suggest doing so without delay, there is only a finite amount of time for underwriters to assess your presentation and present an alternative.

Key themes to expect in the forthcoming renewal period

- Rate increases from all leading insurers – costs likely to rise;

- Insurer appetite to grow portfolios remains limited, particularly with practices that undertake a significant amount of property work;

- Extensive information requests continue – you can expect additional questionnaires, including on the impact of Covid-19 on the business;

- Select insurers are introducing personal guarantees for practices that are a limited company or LLP;

- Obtaining quotations is taking longer, particularly when approaching alternative insurers;

- It is vital to have a complete presentation (including up-to-date claims summaries) ready four to six weeks before the renewal date; and

- It is imperative to undertake a thorough review of the market.

Should you wish to seek a second opinion, please do get in touch. We would be delighted to assist and provide an objective assessment of your arrangements, and help you add real value to your renewal process this year.

We were delighted to welcome 260 new clients in 2020, with firms ranging from top 50 practices to sole practitioners. the majority of whom engaged with us seeking a second opinion having been unaware of our ability to approach insurers that their incumbent brokers were unable too.

To repeat, please do not leave it too late. If you have not already commenced your renewal process, please do so without delay. The clock is ticking and, in the prevailing insurance market conditions, you want to ensure that you have maximum options available to you.

To contact Marc Rowson, call 020 7933 2034 or email marc.rowson@uk.lockton.com [2]