By Mark Cardy, Chartered Financial Planner at Benchmark Financial Planning, a member of Legal Futures Associate, SIFA Professional

By Mark Cardy, Chartered Financial Planner at Benchmark Financial Planning, a member of Legal Futures Associate, SIFA Professional

The scenario

Carole is aged 85 and has ongoing health issues. She has no children and has never married so would like her younger brother to have her home when she passes away. She would like access to her investments should she need them and is looking for ways to mitigate Inheritance Tax (IHT) on her estate. She spoke to her solicitor for help, who approached Benchmark Financial Planning who have financial planners that specialise in this area.

Initial comments

Carole and her solicitor recognised that this situation needed careful planning to help her achieve her desired outcome. As a Chartered Financial Planner, Mark Cardy, who is also Society of Later Life Advisers (SOLLA) accredited and an Affiliate of the Society of Trust and Estate Practitioners (STEP), has a wealth of experience in this area. However, it’s always important to remember that every situation is unique.

Given that Carole could potentially be vulnerable due to her age and health, Mark took great care to take the process step by step over a number of meetings involving her younger brother throughout to provide additional emotional and practical support. This included an initial meeting without obligation or fee, followed by the completion of a fee agreement prior to any chargeable work being completed. Once a detailed report was drafted, Mark took the time to run through this in a further face to face meeting and allowed time for Carole to digest this information before following up. Particular care was taken to clearly disclose and explain all initial and ongoing fees that would be incurred by following the advice provided. Equally, the risk and potential losses involved with any investment recommendation were quantified and explained in detail.

Although Carole’s primary concern seemed to be around IHT, Mark, whilst sensitive to her concerns, highlighted the primary importance of investment planning rather than letting tax drive the process. Mark acknowledged the importance of the client’s objectives, preferences and timescales whilst taking time to challenge assumptions and highlight shortfalls where appropriate. Ultimately, having an open discussion about the available options and begin to think about the relative merits and drawbacks of each was key.

By taking the time to collect information and fully understand her situation and objectives, Mark was able to carry out detailed research into a range of options in order to establish the most suitable solution and then proceed with a recommendation. This was aided by a close working relationship with Carole’s solicitor built up over a number of years, meaning that ideas and information (with Carole’s consent) could be shared and discussed. This collaborative approach with the solicitor enabled any questions and considerations to be dealt with in real time which was a great benefit to everyone involved. Most importantly, Mark’s approach gave Carole and her brother real peace of mind.

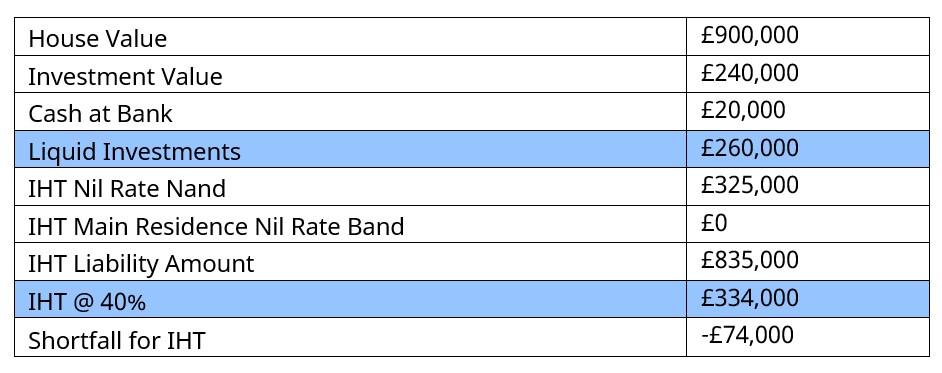

Situation Review

Mark’s initial calculations showed that the current investments Carole held did not cover the potential IHT liability on death. Therefore, if no action was taken, Carole’s brother would potentially be unable to pay the tax bill without selling the property (depending on the investment value at death and the terms of the will ):

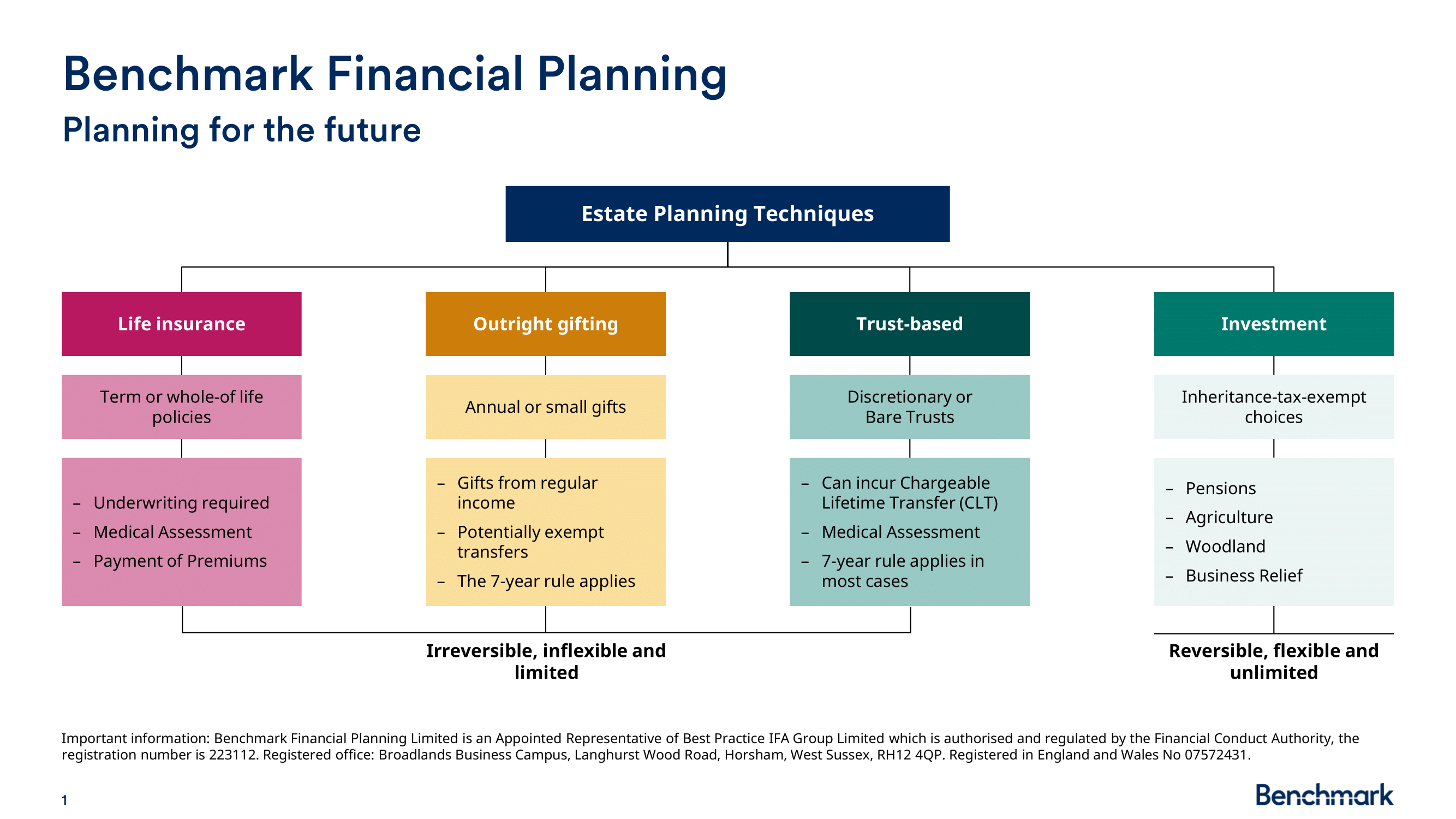

Overview of options considered

We reviewed four options considered to be broadly appropriate in this situation taking into account Carole’s current capacity, potential vulnerabilities and health, potential life expectancy and objectives:

Life insurance

The simplest option was to set up a life insurance policy designed to pay the IHT liability on death. However, an initial underwriting enquiry with basic details showed that this would not be possible due to Carole’s health issues.

Outright gifting

Using a gift to mitigate IHT requires the donor to survive 7 years for this approach to be successful. Due to Carole’s health, it wasn’t clear that this would be the case, so this option was disregarded.

Trusts

Any trust Carole set up would also require that she survives 7 years to effectively be successful, so this option was also disregarded.

Investments

Using an investment that qualifies for Business Property Relief (BPR) for Carole’s portfolio would give 100% IHT relief in 2 years. That 2-year clock would start ticking as soon as the investment is made.

BPR is a well-established mechanism designed to stop small family businesses effectively having to deal with 40% tax on death, potentially resulting in forced closure and redundancies. Although many solicitors have heard of BPR, advising on these types of investments is an FCA regulated activity and very few solicitor firms hold the necessary permissions to provide advice.

BPR investments are generally considered to be high risk as the companies involved have to be of a smaller size to qualify for this relief. It’s important to consider for each individual whether they have the risk appetite and capacity for loss to invest in such a scheme. There are many BPR investment schemes of varying quality so regulated advice from an experienced professional is key. Whilst BPR investments are generally high risk not all are as volatile as the wider Alternative Investment Market (AIM) and some have weathered recent market conditions well.

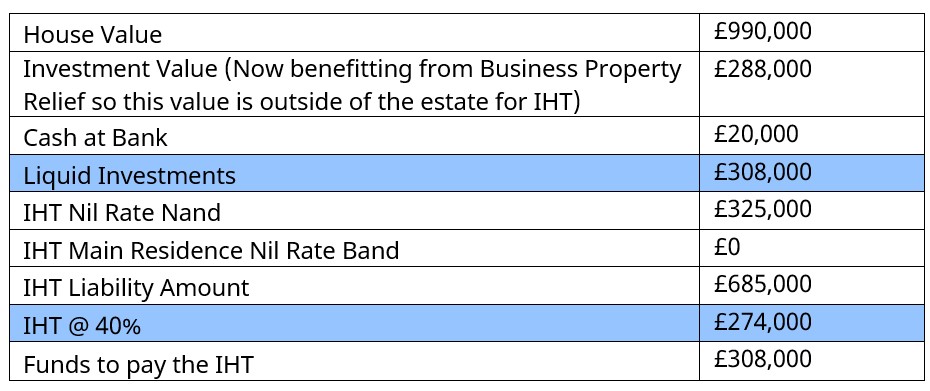

Outcome

As a result of Mark’s advice, the performance of the investment selected and Carole surviving two years, she was in a far better position to cover the potential tax liability (assuming all else remains equal and the investments are not drawn from in the interim):

It is worth noting that any IHT liability will need to be paid before probate is granted which could cause an issue should the beneficiary not have access to sufficient savings of their own. That said, the tax charge could potentially be paid direct to HMRC from the BPR investments subject to the investment provider’s permission.

By working closely with Carole and her solicitor, Mark was able to put a suitable solution in place and ensure a ‘joined up’ approach encompassing the updating of Carole’s Will and Power of Attorney. This, reinforced by Benchmark’s ongoing annual Wealth Service ensures Carole’s arrangements remain suitable and that she continues to be well informed. BPR investments are accessible should she need access to money; however, further advice would be provided before any withdrawal.

This ongoing relationship also has the potential to lead to a number of introductions to friends and family for both Mark and the solicitor.

This financial advisory company is listed on the SIFA Professional Directory of financial advisers (South East Region) – to view their details please Click Here

Important Information: This client example is for case study purposes only and may not represent a typical client. For the purpose of the case study some data has been omitted such as budgetary data.

The value of investments may go down as well as up and investors may not get back the amounts originally invested. Levels and basis of tax rates and reliefs are subject to change.

This communication is intended to be for information purposes only, for professional clients and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Benchmark Financial Planning does not warrant its completeness or accuracy. Benchmark Financial Planning is not responsible for the accuracy of the information contained within linked sites. No responsibility can be accepted for error of fact or opinion. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions.

Benchmark Financial Planning is an Appointed Representative of Best Practice IFA Group Limited which is authorised and regulated by the Financial Conduct Authority, the registration number is 223112. Registered office: Broadlands Business Campus, Langhurst Wood Road, Horsham, West Sussex, RH12 4QP. Registered in England and Wales No 07572431.