By David Turner, Director and Chartered Financial Planner at Gresham Financial Strategies Ltd, a member of Legal Futures Associate, SIFA Professional.

By David Turner, Director and Chartered Financial Planner at Gresham Financial Strategies Ltd, a member of Legal Futures Associate, SIFA Professional.

The situation …

The following case highlights a problem some clients feel do not have a solution, so I am keen to share with you how a solution can be achieved resulting in a satisfied client. Whilst this client did not come from a solicitor referral, it could easily have done so.

I was recently approached by a prospective client to review their pension situation and options as the client was keen to take retirement at 63, a couple of years ahead of the employer scheme retirement age.

The client explained he was unmarried, though he and his long-term partner had been considering getting married for some time. They have an adult married child (now more or less financially independent) but who is hoping to move to a larger property soon as she is starting a family and could do with £20,000 to £30,000 to ease the costs. The clients own their house, now valued at £650,000, with no mortgage.

The client has an aged mother who may need some assistance in future, but the extent and amount is unknown. The client, his partner and their child are in good health. The client has an old will dating back over 20 years; his partner had no will.

The clients require an income of about £2,000pm, net of tax to maintain their standard of living and a risk assessment questionnaire showed both reasonably accepting of risk, the client more so than his partner. If possible, the clients would like to leave their daughter and grandchild an inheritance and would like the flexibility to provide some financial assistance to the client’s mother, should this be necessary, though this is considered unlikely.

A final salary pension scheme with an expected pension of £15,000pa is due to the client at 65 and two State Pensions of £10,000pa (client) and £8,000pa (partner) are due at age 66. The final salary scheme pays increases of 5% pa and a spouse’s pension of 66%. Combined the pensions will provide sufficient income from 66 onwards, but there is an “income gap” in the intervening years.

The clients have accumulated £150,000 of cash savings (£80,000 of which is in a range ISAs) and the client has a pension fund of £400,000 in his employer’s trust based money purchase scheme; his partner has £16,000 saved in a personal pension. In this case, a pension was not available from the employer money purchase pension scheme, which meant employees had to search for an ‘annuity’ provider or transfer the accumulated pension fund out to another scheme in order to obtain a regular pension payment.

They need £25,000 to replace their car, but no other capital is required.

Advice and Actions

- Do not draw the final salary pension until 65 to avoid early retirement penalties and to retain the guarantees and security implicit in a final salary scheme.

- To ensure that the partner receives a widow’s pension should the client pre-decease his partner, they decided to marry.

- Some consideration was given to transferring the final salary scheme to a pension in the client’s name but rejected as this would involve losing the underlying guarantees and security of income from 65.

- We researched annuity purchase options for the £400,000 pension fund, but rejected this option for the time being, preferring to wait until the client is older when annuity rates might be higher, or if they face health issues when an impaired life annuity could be a better option. Annuity purchase now also would mean locking into an income which might not be required in 2 or 3 years’ time. Furthermore, if the client dies the fund could pass to his now wife and/or daughter, which might not be possible if an annuity had been purchased, though a 5 year guarantee on the annuity would provide some protection, as might a life assurance policy.

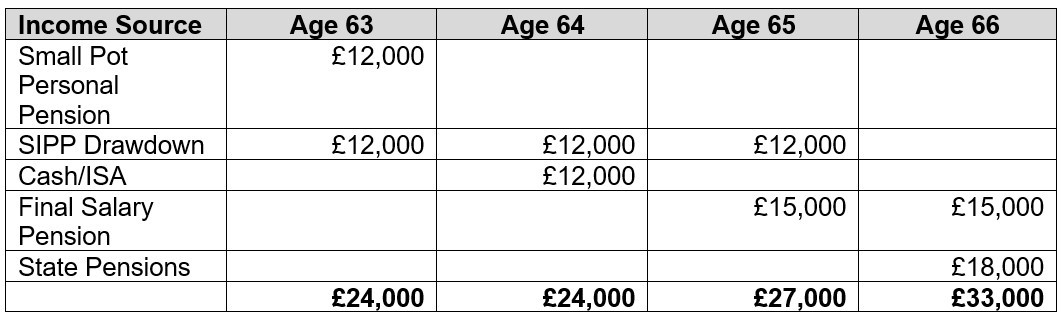

- To meet the income gap over the next few years

- Encash the £16,000 personal pension using the “small pots rule” to draw £4,000 tax free cash and a single income payment of £12,000. Although this will be taxed initially, the tax can be reclaimed as the client’s wife has no other income.

- Switch the client’s employer money purchase scheme of £400,000 to a Self Invested Personal Pension (SIPP) from which drawdown of £100,000 can provide cash of £25,000 to purchase the replacement car and income payments of about £12,000pa (i.e. keeping income just below the threshold for income tax) topping up as necessary from cash and ISA savings.

- Within the new personal pension set aside sufficient cash in the crystallised section (i.e. the part of the pension that has already started to have withdrawals taken from it) of the fund that to meet the likely income requirements in the next few years. This should avoid becoming forced sellers in times of market instability.

- The balance of the crystallised section and the uncrystallised section are invested into a broadly based portfolio of funds aligned to the client’s medium/long term objectives and appetite for investment risk. Asset allocation and underlying fund selection will be reviewed 6 monthly.

- Once the final salary and State Pensions come into payment drawdown payments can be reduced, or ceased, as necessary.

- As on the client’s death the pension fund could be required to support his wife, so set up a 5 year renewable term assurance policy in trust to their child. At each 5 year anniversary of the plan, discuss whether the term assurance is still required and if so the plan can be renewed without medical underwriting.

- The client and wife were advised to set up new wills reflecting their current circumstances and wishes and were referred to a known solicitor we work with.

- With income secured the clients can consider passing capital to their child using the £4,000 from the wife’s personal pension and cash reserves.

- Cash reserve could also be used to fund ISAs for a couple of years, maximising the tax efficiency of investments.

- The SIPP and ISAs were placed on the same investment platform to reduce fees and record keeping.

- Looking further ahead, if income requirements cannot be met from the pensions and savings the clients will be able to consider equity release against their property.

Hopefully the above demonstrates that whilst retirement planning can and is a complex business, identifying that there may be a solution to most problems, and referring to a trusted qualified professional, should end with a mutually satisfied client.

This financial advisory company is listed on the SIFA Professional Directory of financial advisers (London Region) – to view their details please Click Here