![]() Aaron and Partners look at incorporation and the pros and cons of your options.

Aaron and Partners look at incorporation and the pros and cons of your options.

So, you want to incorporate? Incorporation provides limited liability and that is really useful. With a few exceptions, it means that a business failure may not affect your personal assets. It provides a vehicle for others to invest in your business and enables you to give a stake to key staff. It can also be tax efficient in some circumstances.

The first question to decide is whether to become a limited company or a limited liability partnership (LLP).

There are pros and cons to each and you need to think about the key elements of your business before you jump in – it’s not easy to change your mind later.

The key differences between limited companies and LLPs are around management and tax.

A limited company has directors and shareholders. Shareholders own the business and are rewarded by dividends if the company makes a profit and by an increase in the value of the shares if the company becomes worth more. The shareholders appoint the directors who run the business. The shareholders only have the right to veto key decisions and have limited rights to information and no right to run the business on a day to day level. A majority of shareholders can remove the directors.

An LLP has members (often referred to as partners) who both own and have a right to run the LLP. There is no difference between owners and mangers in an LLP, although separate rights can be artificially created, in the same way that shareholders can be granted management rights in a limited company. Both structures require a detailed constitution document – a Members’ Agreement for an LLP and a Shareholders’ Agreement for limited company.

The second issue is around tax. A company is taxed on its profits and pays corporation tax, currently at 20% reducing to 17%, on its profits. The directors are employees and are paid salary under PAYE and the company pays employers’ National Insurance at 13.8% on their salaries. Shareholders can take dividends out of profits which are taxed at dividend rates.

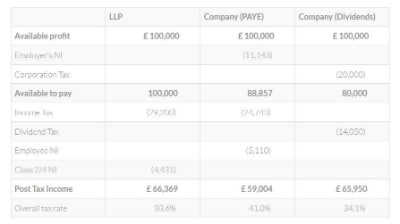

A simple view of the difference in tax is as follows (please remember that this is just an example at one profit level and that individual’s circumstances will differ and you need professional tax advice from your accountant):

There may also be issues around pension contributions which need to be from relevant income and dividend income may not count for tax relief. Because directors are employees, benefits are also taxed.

If a company is making large profits which the owners do not need to extract, it is often better to shelter them in a limited company, having paid 20% tax, whereas if the owners remove all the profit each year, then an LLP can be more tax efficient.

There are other differences which will make a difference to your choice. Limited Companies can have tax efficient share schemes, which can be good for incentivising employees, especially if a sale is planned. However, in an LLP, especially one providing professional services, it is easy to make senior employees into members (it usually requires a capital contribution, but the firm can generally arrange the funding) saving the business 13.8% Employers NI and making them self employed which is usually an advantage.

LLPS have more flexibility, as there is no need to keep set amounts of capital and it is easy to change the capital between members from year to year.

When it comes to people leaving, an LLP is again more flexible. A retirement can be done with a s short, simple deed of retirement. In a limited company, there can be a lot of paperwork, especially if the company decides to buy back the leaver’s shares.

I was recently instructed on two similar jobs; both were small firms where an older partner was retiring and the younger partners were continuing. One was an LLP and the other a limited company. For the LLP I drafted a four page deed of retirement and for the limited company I drafted 14 different documents!

The final issue to consider is that of culture. What feel do you want your organisation to have? Is it a collegiate style where everyone works together or a more corporate style with command and control? Again, there is no right and wrong – you need to decide.

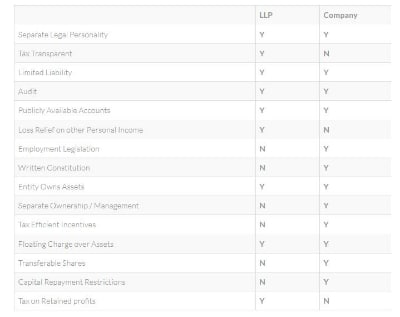

In conclusion, the structures can be compared below:

Please get in contact with our Professional Practices team, using the contact details below, if you would like to discuss any of the issues raised in this article. This article is intended for advice only and may not reflect your particular personal and business needs; you should not rely on it.