By Mark Cardy, a SOLLA Accredited, STEP Affiliated and Chartered Financial Planner with Benchmark Financial Planning, a member of Legal Futures Associate, SIFA Professional.

By Mark Cardy, a SOLLA Accredited, STEP Affiliated and Chartered Financial Planner with Benchmark Financial Planning, a member of Legal Futures Associate, SIFA Professional.

Clients whose estate exceeds the RNRB

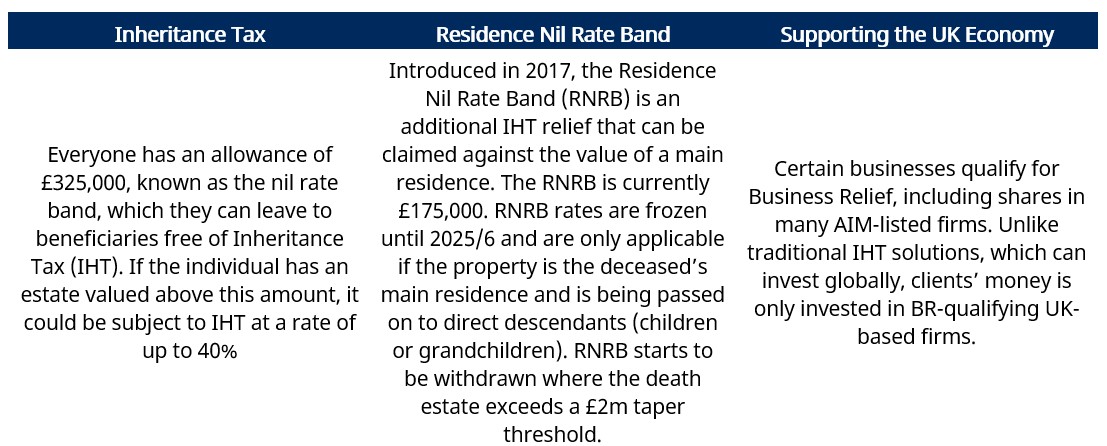

Clients with an estate worth more than £2 million face a tapered residence nil-rate band (RNRB) allowance. This means that it will lose £1 of RNRB for every £2 that exceeds this £2 million threshold. This planning scenario explains how Business Property Relief (BPR) can help restore the RNRB for large estates as well as reducing the amount of IHT payable overall.

Meet Eve

Eve is 83. She is widowed, with two children and four grandchildren. Her estate is worth £2.4 million. Eve understands that her grandchildren should be able to make use of the RNRB when she passes away. The RNRB is an additional allowance of £175,000, on top of the £325,000 nil-rate band (NRB), that is assigned specifically to the value of the family home. As Eve inherited her husband’s estate when he died, her estate will benefit from two NRBs and two RNRBs.

Eve is 83. She is widowed, with two children and four grandchildren. Her estate is worth £2.4 million. Eve understands that her grandchildren should be able to make use of the RNRB when she passes away. The RNRB is an additional allowance of £175,000, on top of the £325,000 nil-rate band (NRB), that is assigned specifically to the value of the family home. As Eve inherited her husband’s estate when he died, her estate will benefit from two NRBs and two RNRBs.

However, the value of the RNRB is tapered for estates valued at more than £2 million. So, Eve will lose £1 of her £350,000 RNRB for every £2 that her estate exceeds the taper threshold.

Eve’s adviser explains that the value of her estate is assessed on the day she dies, so lifetime planning could restore the value of the RNRB. Eve could set up a trust right now, which would immediately solve the RNRB problem. However, it would trigger a chargeable lifetime transfer at 20% above the NRB. Plus, further inheritance tax would be payable if Eve died within seven years.

In conjunction with this advice, Eve is referred to a solicitor to review her will and Power of Attorney.

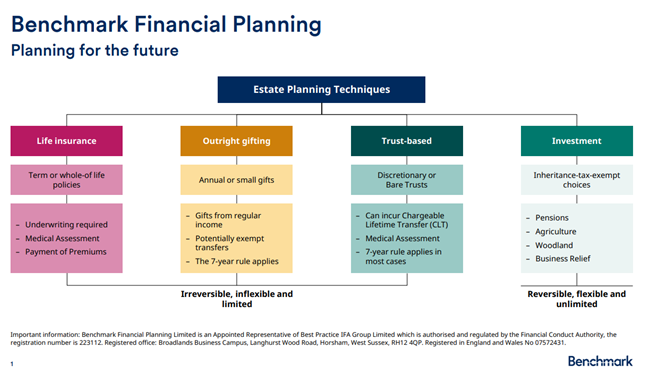

Overview of options considered

We reviewed four options considered to be broadly appropriate in this situation taking into account current capacity, potential vulnerabilities and health, potential life expectancy and objectives:

Life insurance

The simplest option was to set up a life insurance policy designed to pay the IHT liability on death. However, an initial underwriting enquiry with basic details showed that this would not be affordable.

Outright gifting

Using a gift to mitigate IHT requires the donor to survive 7 years for this approach to be successful. It wasn’t clear that this would be the case, so this option was disregarded.

Trusts

Any trust set up would also require the donor to survive 7 years to effectively be successful, so this option was also disregarded.

Investments

Using an investment that qualifies for Business Property Relief (BPR) would give 100% IHT relief in 2 years. That 2-year clock would start ticking as soon as the investment is made.

BPR has evolved since its inception and is now a popular way to minimise tax deduction following a death or on lifetime gifts. For example, a 2013 decision allowed investors to hold BPR-qualifying, AIM-listed shares in an ISA, making them even more tax efficient. It’s likely it will continue to change in the future – hopefully, for the benefit of inheritors. Although many solicitors have heard of BPR, advising on these types of investments is an FCA regulated activity and very few solicitor firms hold the necessary permissions to provide advice.

BPR investments are generally considered to be high risk as the companies involved have to be of a smaller size to qualify for this relief. It’s important to consider for each individual whether they have the risk appetite and capacity for loss to invest in such a scheme. There are many BPR investment schemes of varying quality so regulated advice from an experienced professional is key. Whilst BPR investments are generally high risk not all are as volatile as the wider Alternative Investment Market (AIM).

Outcome

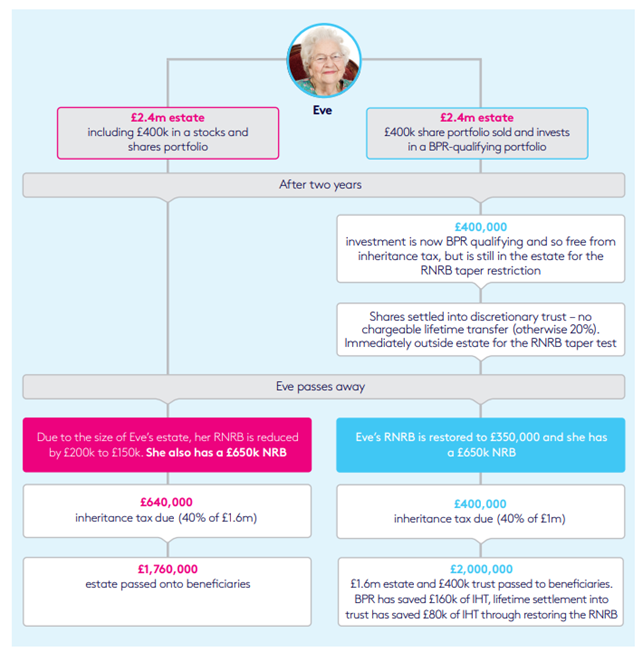

The adviser assesses Eve’s objectives, appetite for risk and capacity for loss and deems her suitable for an investment that qualifies for BPR and recommends she invests £400,000 in a BPR-qualifying portfolio. If she holds this for at least two years, it can be left to her grandchildren free from inheritance tax when she dies. The value of the portfolio will be considered when calculating the RNRB taper threshold. So, Eve’s adviser recommends that after she has held the portfolio for two years, she settles it into a discretionary trust. This would immediately remove the value of her portfolio from her estate for the purpose of the RNRB taper test. At this point the portfolio would qualify for BPR, meaning no chargeable lifetime transfer should be payable.

When Eve dies, no further inheritance tax should be payable on the amount settled into trust, even if she dies within seven years – as long as the trust continues to hold the investment.

Settling BPR-qualifying shares into a discretionary trust after two years restores the value of the RNRB, as well as saving inheritance tax on the value of the investment.

How it works in practice

Let’s see how it might look if Eve were to sell £400,000 of her existing share portfolio and invest in a BPR qualifying portfolio. After two years she could settle the investment into trust, which would bring her estate below the £2 million RNRB taper threshold:

Note: This comparison assumes no loss or gain on any of the investments, although fluctuations will apply in practice. It also doesn’t take into account the initial and ongoing fees investors would pay when buying, selling or reinvesting which would also need to be considered. It’s important to remember that the risk profile of each portfolio, costs and any investment growth or losses are likely to differ.

Advantages of BR

- Can help preserve a family’s wealth

- Only takes 2 years to qualify – Shares must be held at the time of death

- Can be gifted (to reduce value of estate)

- BR assets can replace each other

- Clients retain access to capital

- Inherited ISA Allowance

- Additional permitted subscription (APS)

- Clients retain access to capital

- Transfer into Trust – If the shares were already held for 2 years before the transfer into trust, the potential lifetime charge to IHT is reduced from 20% to zero

- Transfer by way of gift – If the individual (donor) holds BR-qualifying shares for 2 years before gifting, and the recipient of the gift still holds the shares at the time of the donor’s death, the investment retains IHT exemption for the donor (reduce estate)

Risks

Due to the potential for losses, the Financial Conduct Authority (FCA) considers these investments to be high risk.

What are the FCA key risks?

- You could lose all the money you invest.

If the business you invest in fails, you are likely to lose 100% of the money you invested. Most start-up businesses fail.

- You are unlikely to be protected if something goes wrong.

Protection from the Financial Services Compensation Scheme (FSCS), in relation to claims against failed regulated firms, does not cover poor investment performance. Try the FSCS investment protection checker. (https://www.fscs.org.uk/ check/investment-protection-checker) Protection from the Financial Ombudsman Service (FOS) does not cover poor investment performance. If you have a complaint against an FCA-regulated firm, FOS may be able to consider it. Learn more about FOS protection. (https://www.financial-ombudsman.org.uk/consumers)

- You won’t get your money back quickly.

Even if the business you invest in is successful, it may take several years to get your money back. You are unlikely to be able to sell your investment early. The most likely way to get your money back is if the business is bought by another business or lists its shares on an exchange such as the London Stock Exchange. These events are not common. If you are investing in a start-up business, you should not expect to get your money back through dividends. Start-up businesses rarely pay these. (https://www.financial-ombudsman.org.uk/consumers)

- Don’t put all your eggs in one basket.

Putting all your money into a single business or type of investment for example, is risky. Spreading your money across different investments makes you less dependent on any one to do well. A good rule of thumb is not to invest more than 10% of your money in high-risk investments. (https://www.fca.org.uk/ investsmart/5-questions-ask-you-invest)

- The value of your investment can be reduced.

The percentage of the business that you own will decrease if the business issues more shares. This could mean that the value of your investment reduces, depending on how much the business grows. Most start-up businesses issue multiple rounds of shares. These new shares could have additional rights that your shares don’t have, such as the right to receive a fixed dividend, which could further reduce your chances of getting a return on your investment. If you are interested in learning more about how to protect yourself, visit the FCA’s website. (https://www.fca.org.uk/investsmart)

This financial advisory company is listed on the SIFA Professional Directory of financial advisers (South East Region) – to view their details please Click Here

Important Information: This client example is for case study purposes only and may not represent a typical client. For the purpose of the case study some data has been omitted such as budgetary data.

The value of investments may go down as well as up and investors may not get back the amounts originally invested. Levels and basis of tax rates and reliefs are subject to change.

This communication is intended to be for information purposes only, for professional clients and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Benchmark Financial Planning does not warrant its completeness or accuracy. Benchmark Financial Planning is not responsible for the accuracy of the information contained within linked sites. No responsibility can be accepted for error of fact or opinion. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions.

Benchmark Financial Planning is an Appointed Representative of Best Practice IFA Group Limited which is authorised and regulated by the Financial Conduct Authority, the registration number is 223112. Registered office: Broadlands Business Campus, Langhurst Wood Road, Horsham, West Sussex, RH12 4QP. Registered in England and Wales No 07572431.