By Josh Richardson, Managing Director and Chartered Financial Planner at Informed Financial Planning, a member of Legal Futures Associate, SIFA Professional

By Josh Richardson, Managing Director and Chartered Financial Planner at Informed Financial Planning, a member of Legal Futures Associate, SIFA Professional

We are helping increasing numbers of clients mitigate their Inheritance Tax (IHT) liability. With minimal legislative changes over recent decades, more people now accidentally fall into the bracket.

I say ‘accidentally’ as the clients we help are rarely entrepreneurs or lottery winners. Rather, we are helping ordinary families who have liabilities due to rapidly rising house prices, surplus income from final salary schemes and sensible investing.

Generally, we’re helping clients whose assets or income has grown faster than the IHT allowances, which isn’t difficult considering the nil rate band hasn’t increased since April 2009.

The following is a prime example of the above. Originally referred by a local solicitor, due to the involvement of investments, we stepped in to provide advice on the numerous assets owned by the client.

Case Details

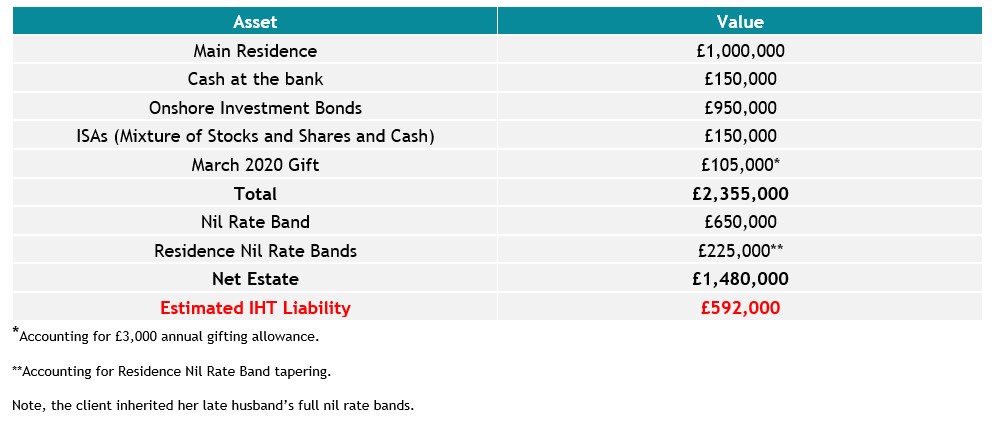

The client, a widow, who held full capacity but was assisted by her son, had assets as follows:

Alongside a large IHT liability, the client had other issues which were complex, but not uncommon, making mitigation difficult:

- She was approaching age 90.

- She received high levels of guaranteed, inflation linked, pension income. Amounting to around £80,000 gross pa.

- She saved surplus income of c.£3,600 per month.

- She was subject to the Residence Nil Rate Band (RNRB) tapering.

Perhaps most importantly, the client’s investment bonds were pregnant with gain. Having held these investments, untouched, for 30+ years, the income tax charge on death was estimated in the region of £175,000.

Should the client have passed away, her estate administrators were likely to settle a joint tax bill of circa £767,000.

Our Recommendations

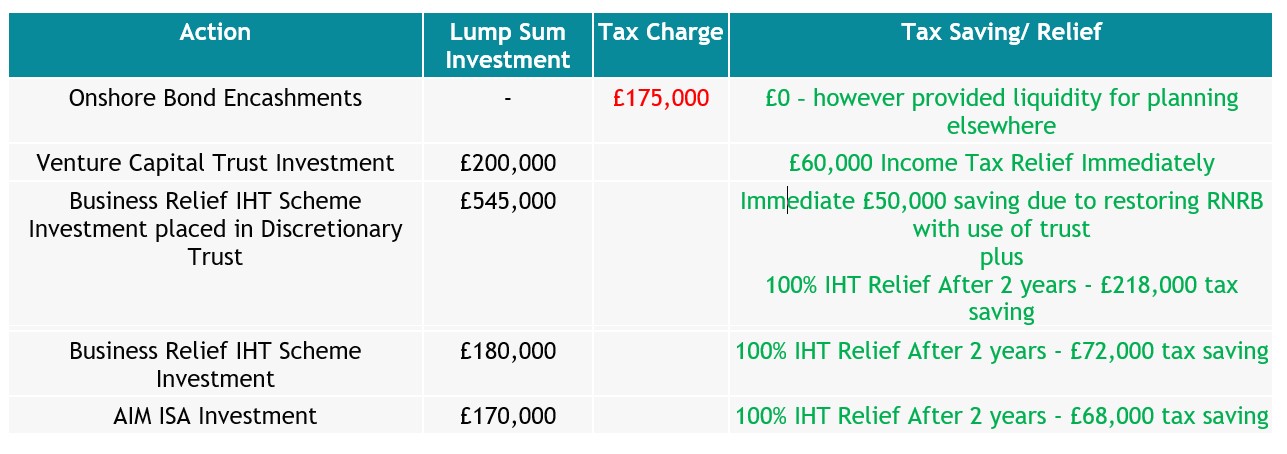

Investment bonds

Encashing the bonds fully would give rise to a large income tax bill, pushing her into the 45% tax band and also leading to the loss of her personal allowance.

However, due to these bonds being subject to IHT and inevitably a large income tax bill on death, it was preferred by the client to try and utilise these assets for IHT planning where possible.

Therefore the recommendation was made to encash these entirely.

Income Tax Relief

To mitigate the income tax liability upon encashment of the bonds a recommendation was made to invest £200,000 in a Venture Capital Trust, to secure £60,000 of income tax relief.

Whilst ordinarily needing to be held for a minimum of 5 years to secure this relief, should the client die within this period, the tax relief is not reclaimed by HMRC.

This therefore secured a significant reduction to her income tax liability regardless of any life expectancy concerns.

Inheritance Tax Position

Naturally, the VCT offers no additional IHT benefits, therefore this liability had to be tackled with other planning.

Due to her age and family issues, the client did not wish to consider direct gifts or gifts into trust. A wait of 7 years for ‘success’ did not appeal to her.

Whilst Whole of Life insurance was considered, due to her age, no provider would offer terms.

The recommended route was therefore to:

- Invest £545,000 into a Business Relief (BR) IHT scheme, with £325,000 to be placed immediately into a discretionary trust.

- Invest £180,000 into a second BR IHT scheme, to be retained personally.

- Transfer all ISAs and contribute £20,000 into an AIM Investment ISA.

The client was accepting of all risks associated with the BR, AIM and VCT products due to the tax benefits afforded to her.

Whilst she was reluctant to utilise trusts, the ability for part of the first recommendation to fall outside of her estate within 2 years was attractive.

Additionally, the use of a trust constituted an immediate gift for RNRB tapering purposes. Whilst BR products are still included in the calculations, this gift into trust allowed the client to fully restore her RNRB. This provided an additional, immediate, IHT saving of £50,000.

Tax Savings and Timescales

Ultimately, should the client pass away within 2 years from implementation of advice, she will have saved around £110,000 in varying taxes. Should she survive beyond two years, the overall saving will rise to circa £468,000.

Alongside the above, gifting strategies, such as gifts out of regular income are also being used to ensure the client’s problem does not increase further.

Ideal Scenarios

The above highlights the complexities of IHT mitigation.

Early planning is key.

For clients who are younger, there are wider options available:

- Whole of life insurance, written correctly into trust

- Direct gifting

- Gifting into trust such as absolute, discretionary, or flexible reversionary trusts etc

- Business relief investments

- Pension contributions and the use of pensions as a legacy

There is no ‘one solution fits all’ for IHT. Clients’ objectives, views and family situation will dictate the appropriate recommendations.

However the message remains the same, the earlier a client can plan, the easier they can make it for their beneficiaries on their deaths and the greater the IHT mitigation can be.

This financial advisory company is listed on the SIFA Professional Directory of financial advisers (North East Region) – to view their details please Click Here