![]() By Julian Bryan, Managing Director of Legal Futures’ Associates Quill

By Julian Bryan, Managing Director of Legal Futures’ Associates Quill

This blog is based on our ‘15-Step Guide to Starting Your Own Law Firm’ webinar from 12 November 2020. To download the e-Book we shared with listeners, please visit www.quill.co.uk/Legalpracticemanagementforstartups.

When I set up my first business 20-or-so years ago, I was very nervous but also very excited. I had lots of questions but didn’t always know who to ask them to.

That’s why we created this guide to help you pursue your dreams and set up your own law practice – the right way, with the right tools, and with the right mindset.

“The big trick that law firms play on their staff is trying to persuade them how impossible it is to go solo. This is simply not true. If I can do it, you can do it too. Don’t get put off by the stories. It’s a lot easier than it appears.”

James Brown, Partner, Hall Brown Family Law

In our previous blogs, we covered steps 1 to 3 (opening a bank business account, purchasing Professional Indemnity Insurance and formulating your business plan) and step 4 (building risk management and compliance into the aforementioned business plan). Today’s blog covers steps 5 to 8, namely taking the plunge, formally applying, choosing your business structure and managing client accounts.

WATCH WEBINAR:

Step 5: Take the plunge!

If you’ve weighed the pros and cons and made your decision to move forward with setting up your own law firm – congratulations! This is the start of a great adventure. The old adages ‘you never know until you try’ and ‘you’ll only regret the things you don’t do; never the things you do’ apply here.

Whilst you’re opening a new practice, this doesn’t mean you have to do it all alone.

Starting a firm is feasible if you have the tools and resources in place to help you maximise your fee-earning potential.

“There’s also an abundance of readily available resources – similar to this guide you’re reading. Martin Smith’s book titled Setting Up and Managing a Legal Practice is one such resource,” says James Brown, who started Hall Brown Family Law five years ago.

“And the best resource of all is actually talking to people who’ve done it before you. There’s a wonderful, helpful community of lawyers who’ve started their own firms and will always make time for someone who wants to make the jump too. Reach out to them!

“Walking into your own office on the first day is the most surreal experience. The first time you answer the phone and the first time you record time is incredibly exciting. The first bill being paid is absolutely remarkable as it shows you can turn your ideas on paper into actual money coming into a bank account.”

Initially, you’ll wear many hats and this can distract you from your main goal of providing billable legal services. (Most entrepreneurs we spoke to say to plan for roughly one-third of your time spent on management obligations and two thirds to fee-earning.)

“There is a temptation when opening a new law firm as a sole trader to try and do everything yourself to save costs, but this can be counterproductive if it stops you from doing what you’re good at in generating fees. In some respects, it is more important to recognise what you’re NOT good at, so that you can seek to outsource that to enable you to focus on what you are good at. Let’s put it this way: I’ve never met a solicitor who set up their own practice because they were good at writing up their accounting records.”

Joel Topham, Senior Manager, Sagars Accountants Ltd.

Step 6: Time to formally apply

Another early step is to complete your SRA (or equivalent) firm authorisation application form, otherwise known as the FA1. This document is not for the faint-hearted. Standing at 13 pages, this form requires everything from registration details, turnover predictions, funding sources and shareholdings, roles and responsibilities, specialisms, and PII to money handling and signed declaration.

Without your FA1 form completed and approved by the industry regulator, you can’t begin to practise.

You’ll also need to complete FA2 forms to approve managers, owners and compliance officers unless these lawyers can be ‘deemed approved.’ (The meaning of ‘deemed approved’ is explained in the SRA Authorisation of Firms Rules.) Further, you’ll need to complete an FA10 form if your firm is caught by anti-money laundering legislation.

“The SRA are friendlier than you might imagine. They’re good if you’re straight and transparent with them. If you’re defensive and don’t engage, it gets their back up. You’ll have to complete the FA1, FA2 and FA10 forms to apply; although exclusions apply to the latter two. Then be prepared to answer lots of questions.”

David Gilmore, Director, DG Legal

Authorisation can take up to 16 weeks at its most extreme, but generally, it takes between six to eight weeks.

“Preparing and submitting the application to the SRA is quite a task. But rightly so. Just consider the ubiquitous risks to practices and their end clients. The SRA has a duty, as an industry regulator, to ensure legal professionals are guarding themselves against risks as best they can,” explains Josie Robinson from Josie Robinson Solicitors, who set up her niche specialist medical negligence and sports injury claims practice in 2014.

Along with proof of PII cover, the SRA also like to see your business plan and may ask to see other documents depending on the strength of your application. A head’s up that many of your business decisions addressed in this guide will be showcased in the FA1 form, including how you intend to use outsourced support.

“I needed to show the SRA how I planned to use outsourced support for cashiering and IT as part of this process. Using names familiar to the legal industry assisted my application by satisfying the SRA of my best practice and financial management intentions,” adds Josie Robinson

“Your business continuity plan, risk register and compliance plan are important in formulating your application to the SRA or other regulator. These often don’t get thought through enough,” comments Julian Bryan.

SRA Accounts Rules changes: The SRA Accounts Rules were last updated on 25th November 2019. For guidance on how to operate a client account, apply the rule 2.2 exemption to only hold an office account, maintain a breach register, outline your payment of interest policy, check residual and suspense balances, and make sure your legal accounts software caters for the rules, go to www.quill.co.uk/audit-tips.

DOWNLOAD E-BOOK:

Step 7: Choose your business structure

There are four business models most commonly adopted by sole practitioners:

- Sole proprietorship

- Traditional partnership

- Limited company

- Limited liability partnerships (LLP)

With options 1 and 2, your personal assets are at stake should things go wrong. With options 3 and 4, there’s a greater degree of personal protection, but it’s still not completely bulletproof.

This is a complicated and crucial decision that requires you to engage with the “cautious lawyer” side of your brain. If there’s any point at which it’s worth enlisting outside expertise, this is it. Good accountants are worth their weight in gold. Not only can they help you with this important decision, but they can also discuss the tax implications of each operating model.

“There is no single structure which suits a legal practice better than others. Each has its own pros and cons in relation to tax efficiency, flexibility, risk management and simplicity. Different types of practice will require different structures, as will different owners,” explains Joel Topham. “In most instances, the mid to long term goals of the practice will determine the correct structure for the practice and this may include planning to change structure part way through this period!”

With the right advice upfront, getting the right structure will usually pay for itself in the medium term (and hopefully pay for the advice needed to set it up as well).

You’ll also need your family on board with the proposed business model, as your personal assets are theirs as much as yours.

“Speaking of family, some accountants who are inexperienced with law firms will encourage lawyers to include spouses as partners for tax saving purposes. This practice is strictly prohibited with the SRA unless the firm is a licensed body,” warns David Gilmore.

Alternatively, you may actually be starting this business with partners. If that’s the case, make sure to draw up clear and formal agreements that cover practicalities such as profit-sharing, holiday entitlements, decision-making roles, termination of under-performers, partnership exits and succession planning.

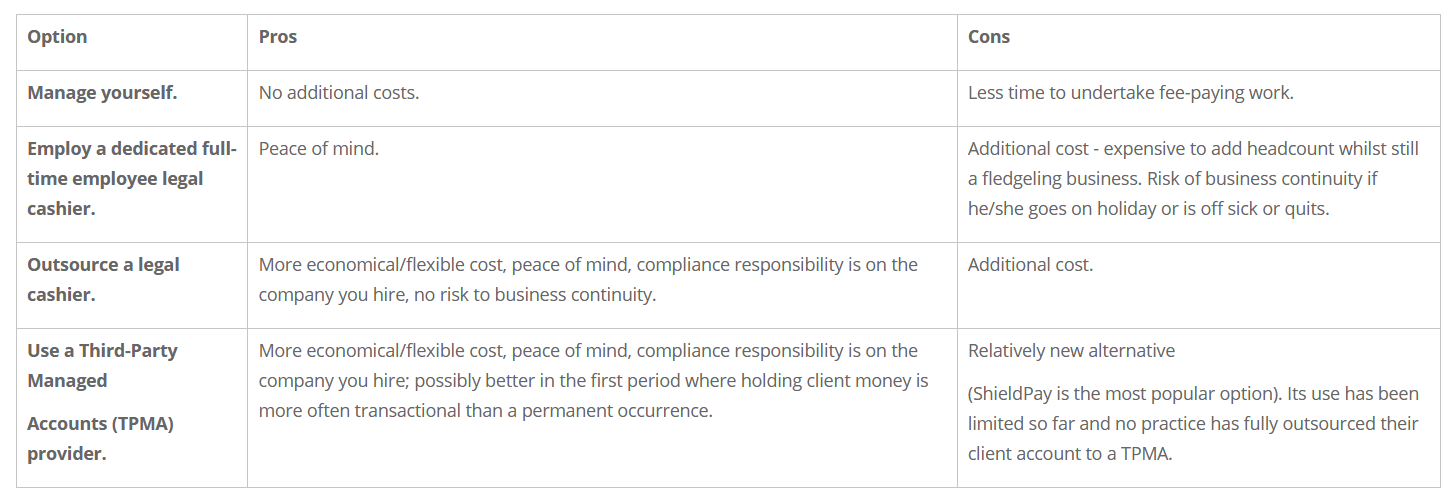

Step 8: Decide how to manage your client accounts

You must ensure your clients’ money is clearly identifiable as theirs. Typically, this means holding funds in a separate, named client bank account.

“Make sure you don’t spend client money unless you’re allowed to. Understand the SRA Accounts Rules or other regulatory stipulations. As part of maintaining a client account, you’ll need an annual audit by an accountant, unless you have an exemption, and you must keep accounting records. Outsourcing to specialists like Quill means you can rest easy that your records are up-to-date and accurate always,” states Joel Topham.

The next important question is: How you are planning to operate this client account?

“The cost-saving advantages [of outsourcing] are substantial when compared to an in-house cashier’s wages and legal accounts software supplied by someone else,” comments Jane Lodeto at Browns Solicitors.

“Remember: the more work you take on with running your business, the less time you’ll have to actually generate more business and undertake fee-paying work. If you are going to employ another to do it for you, this will be an additional cost to the business but the benefits may outweigh the costs,” says Julian Bryan. “Whatever decision you make, it is important that you trust this business as they’re overseeing one of your key regulatory responsibilities.”

To continue reading, visit Legal practice management for start-ups and download free e-Book.

Julian Bryan is the Managing Director of Quill, which helps law firms streamline and run their practice better by providing simple and easy-to-use legal accounting and case management software, as well as outsourced legal cashiering services. Julian is an advocate for quality software standards and served as the Chair of the Legal Software Suppliers Association from 2016 to 2019. He can be reached at j.bryan@quill.co.uk.