The latest research from property legaltech firm Search Acumen points to an elevated number of property transactions for Q4 2025, signalling renewed confidence in the property sector, following years of volatility. Amid these market conditions, consolidation among law firms has notably levelled off, reflecting the sector’s growing capacity to absorb increased caseloads and adapt to evolving transactional demands

The latest research from property legaltech firm Search Acumen points to an elevated number of property transactions for Q4 2025, signalling renewed confidence in the property sector, following years of volatility. Amid these market conditions, consolidation among law firms has notably levelled off, reflecting the sector’s growing capacity to absorb increased caseloads and adapt to evolving transactional demands

Search Acumen’s analysis of HM Land Registry data shows that there were 332,830 property transactions in Q4 of 2025, a 3.09% rise compared to the 322,690 transactions that took place in Q4 2024. While transactions were 0.9% lower than the peak levels seen during the post-pandemic surge in Q4 2022, this robust performance in the final quarter signals renewed resilience in the property market, with transaction volumes defying the typical seasonal slowdown and indicating underlying market strength.

Within this context of improved market performance, the legal sector has experienced a notable deceleration in consolidation throughout 2025 compared to the previous year, even as robust M&A activity characterised the first half of the year.

Source: Search Acumen analysis of HM Land Registry data

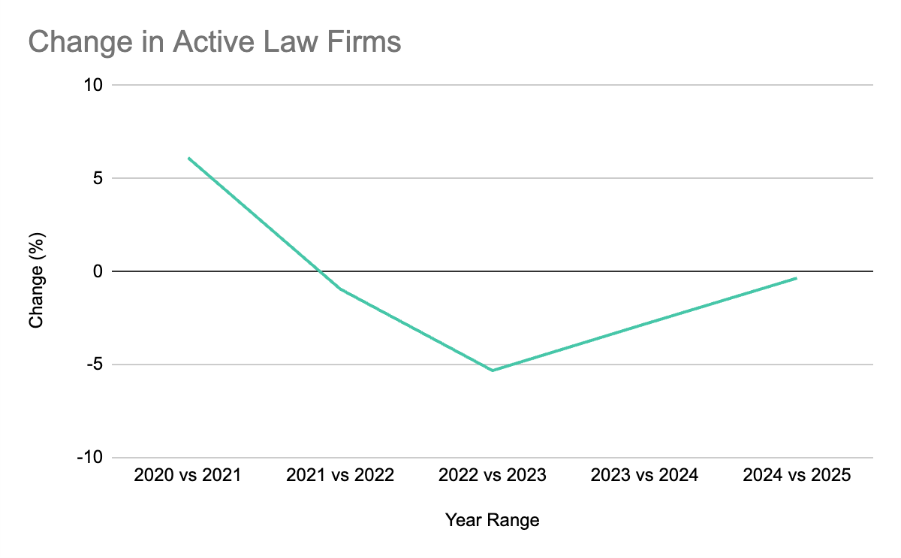

Graph 1: Change in active law firms over time

Market consolidation appears to have stabilised after peaking in 2023, when the number of active firms dropped by 5.32%. The subsequent decreases of 2.82% in 2024 and 0.35% in 2025 suggest a more settled landscape, with fewer firms exiting the market. Over the past decade (2015–2025) the overall number of active law firms has decreased by 13.7%, reflecting sustained structural change within the industry.

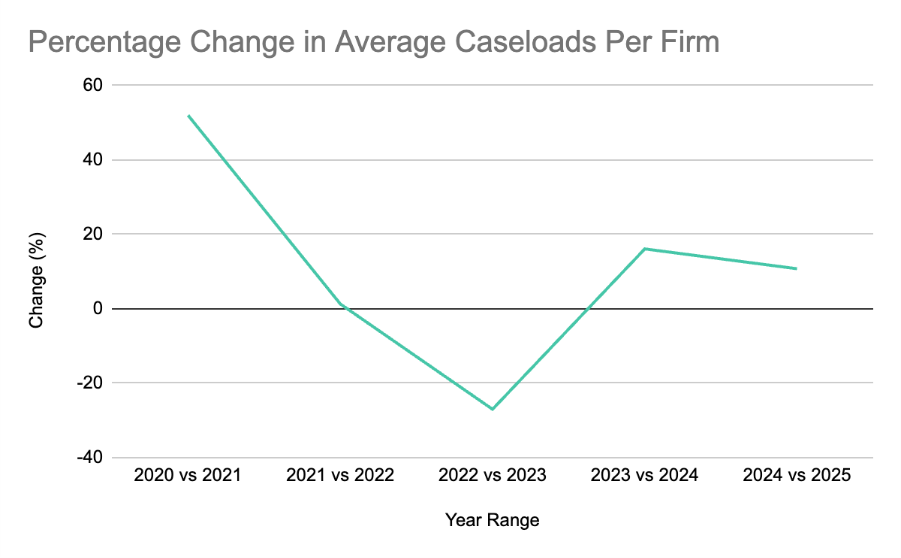

At the same time, the average case load per firm has risen by 5.8% over the last 10 years, highlighting a pronounced shift towards greater concentration of conveyancing activity among a smaller cohort of larger firms.

Source: Search Acumen analysis of HM Land Registry data

Graph 2: Percentage change in average caseloads per firm

The distribution of market share among leading firms continues to exhibit incremental shifts. In Q4 2025, the top five firms accounted for 6.04% of all transactions, a marginal increase from 6% in 2024. Conversely, the collective share held by the top ten firms edged down from 10% to 9.86%, while the top twenty firms saw a slight rise from 14% to 14.14%.

These movements suggest that, while the largest firms are gradually consolidating their market positions, competitive dynamics within the upper tier remain pronounced. The data points to an increasingly balanced distribution of market share among the top ten firms, reflecting ongoing competition and a lack of clear market dominance.

Commenting on the research, Andrew Loyd, Managing Director at Search Acumen, said: “After an unprecedented decade of pressure on the conveyancing sector, it’s encouraging to see transaction volumes end 2025 on a stronger footing, with activity holding up through Q4.

“What’s particularly striking in the latest data is that consolidation now appears to be stabilising; firm numbers are no longer falling at the pace we saw in 2023, yet average caseloads per firm are continuing to rise significantly year on year. That creates real commercial opportunity, but it also reinforces the operational strain on legal teams who are already working hard to meet demand.

“We shouldn’t underestimate the contribution conveyancers continue to make to the wider property market and the UK economy. The sector’s ability to sustain service levels as volumes grow will increasingly depend on further digital innovation. Better data, smarter workflows and automation can support legal professionals, improve resilience, drive efficiency and help reduce cost and complexity for firms and their clients.”